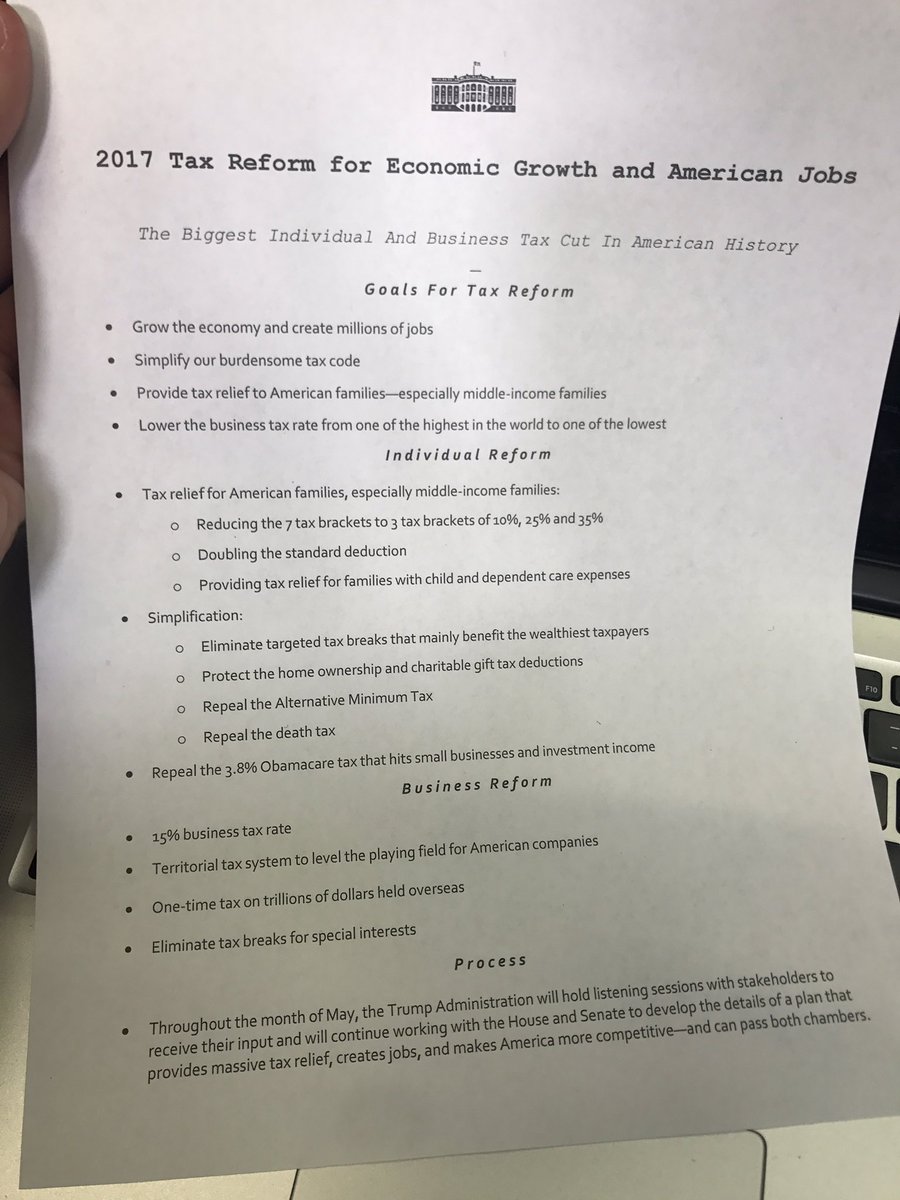

My last post on the 500-word scrawling that has amusingly been called Trump's tax "plan" was quite critical of the proposed 15 percent rate for "business" income, which potentially includes any income that one can contrive to have paid to a business entity (including any state-law entity such as an LLC of which you own 100%), rather than directly to oneself as a wage. I noted that, in practice, this is likely to result in an upside-down rate structure in which rich people commonly pay 15% while their employees pay tax at higher rates. And I noted that it in effect penalizes being an employee who gets paid a salary directly, as if this were a crime that needed to be punished or at least discouraged.

But some readers may have asked: What about the capital gains rate? It was 15% for a while, although it's 20% now. Is the proposed 15% business rate worse than that?

The answer is very clearly Yes. Now, there are some cases in which the 15% capital gains rate works exactly the same way as the "business rate" would - allowing high-earnerrs who have flexibility over cash flow, are well-advised, etc., to get the same result as above. Hedge fund managers can often do this, and it underlies the "carried interest" controversy.

But it's harder to do the capital gains trick than it would be to take advantage of the small business loophole. So less people are able to do it. Plus, there's a whole lot of other stuff mixed in to the capital gains category that has a case for more favorable treatment,

Depending on the particular facts, complicating issues may include the following:

--Capital gain on selling corporate stock gives rise to double taxation if the income is taxed at the corporate level - sometimes a big if.

--There may be nominal inflationary gain mixed in.

--To the extent that capital gain merely reflects earning the normal rate of return on capital, there are arguments for taxing it at a lower rate than that which is economically labor income or rents.

--The capital gains tax is to some extent, and in many cases, a voluntary tax. Hence, the Laffer curve can actually kick in at politically conceivable tax rate levels (e.g., by the time the rate gets into the 30s). This problem is greatly exacerbated by the tax-free step-up in basis for appreciated assets at death, which means the tax can be permanently avoided, rather than merely being deferred. That rule ought to be fixed, but as long as it isn't it constrains how high the capital gains rate should be.

This is not necessarily to defend a 15% or even 20% capital gains rate, especially if we have options at hand beyond just raising the rate, designed (for example) to reduce the feasibility of shoving labor income into the capital gains basket.

But at least we are in the realm of complicated issues and policy tradeoffs - which is not the case with respect to a general 15% "business rate."

It's true that, if we enact a significantly lower corporate rate, it's important to think about the corporate versus non-corporate business tax rate relationship. But (a) the corporate tax is to a degree, albeit imperfectly, more about globally mobile capital than the "business tax," (b) the response should focus on limiting use of the corporation as a tax shelter to escape individual rates on labor income and rents - not extending this problem even further, and (c) corporate income still potentially faces shareholder-level taxation, via the taxation of capital gain and dividends.

Great example of how the "business rate" works: Kansas has idiotically, and to its great detriment, enacted a version of what Trump now wants to do. The Kansas rules actually exempt so-called business income, since state rates are much lower than federal to begin with.

In response, Bill Self, the coach of the Kansas University basketball team, who gets paid $3 million per year, restructured a bit so that 90% of his salary would be "business income' that was exempt from the Kansas income tax. Gruesome details here.

Enacting the 15% business rate, especially in light of Trump's personal stake in the matter (so far as we can understand it despite the lack of transparency), and in light of the Kansas experience, would be straight-out looting and fiscal sabotage, not a policy move that is reasonably debatable or defensible.

Subscribe to:

Post Comments (Atom)

{kind=link}

5 comments:

I'm a bit surprised and underwhelmed that you immediately fixate on a single bullet of a framework and then assume that it will be poorly implemented. Sure, the Republicans don't inspire much confidence, but it seems a bit unfair to assume the mechanics will be identical to Kansas's when there aren't any details yet. Certainly, if they take the Kansas route, the revenue loss would be profound.

I hope you post a broader take on the plan at some point. There's a lot of seemingly foolish red meat in there, but also plenty of base-broadening through reducing tax incentives and doubling the standard deduction that should have bipartisan appeal. Moreover, increasing the standard deduction should also take millions of Americans off the itemizing train, maybe someday making the mortgage interest deduction easier to put on the chopping block.

I'm no Trump fan (I certainly didn't vote for him), but sometimes I think your hyperpartisanship undermines your generally brilliant analysis.

Thanks for your candid comments here. I don't think this is a serious effort by the administration. You'll note that I did not address the DBCFT / Ryan plan in similarly harsh terms, as that's at least potentially a serious idea.

Also, I think it's quite difficult to rein in the "business rate." Even if the worst cases like Bill Self are blocked, there will be a whole lot of self-employed people taking advantage who will be hard to stop, if they establish LLCs and underpay themselves for what the LLC charges and earns. Note the so-called John Edwards Sub S tax shelter that we have these days - which might be struck down at least in some cases if challenged, but the IRS presumably doesn't have the resources.

It might also be appropriate to say something about the serious mis-reporting in the press of what this is on the individual side. Plainly the proposal dramatically reduces rates on people in the top bracket. But the reduction from seven to three brackets does not imply, as the NYT has reported, that this is a tax cut for the middle class. It may or may not be, but we need to know how the new brackets are drawn and which deductions are eliminated. The SALT deduction has bite for middle-income folks, and not just in deep blue states. (E.g., Florida and Texas have high property tax rates and no income tax.) And during the campaign, Trump proposed eliminating the personal exemption amount. It's not clear whether that's included here, but if it is, the overall effect on a family of four taking the standard deduction is higher taxable income from the same AGI under Trump's plan than under current law.

Bottom line: reporting this as an across-the-board tax cut is not correct. It should be reported as a big cut for the wealthy with as yet unclear consequences for everyone else.

Thanks for your blogging on this.

Nice blog.

Thanks for sharing useful information.

tax rates Income

Post a Comment