I just saw (on DVR) the 1931 version of The Maltese Falcon. It's not very good, but fascinating to compare to the classic remake. Much worse acting, pacing, etc., but the cast of characters is exactly the same, and each 1941 performance was so indelible that it's startling to see someone else trying to do what's recognizably, at a general level, the same thing.

Weirdest difference: the Sam Spade character is grinning broadly about 95% of the time. (This was not exactly Bogart's approach - even his smiles are grim.) Best difference: it's pre-Code, so the film is far more candid and explicit re. Spade and Miss Wonderly.

Saturday, April 29, 2017

Friday, April 28, 2017

New article idea

I agreed a couple of months ago to give a talk in Finland on June 1, at the 2017 Annual Conference of the Nordic Tax Research Council. It was planned at the time that I would address the Ryan tax reform plan - meaning in particular the destination-based cash flow tax (DBCFT) - for my northern European audience that can only watch U.S. developments from afar. I'm also committed to write a very short paper for the Nordic Tax Journal based on the talk.

The DBCFT is of course an interesting topic, and for the above purposes I thought I could reasonably be a consumer at the research stage, and purveyor to my audience in delivering the talk and paper, of the best work that's been done in the U.S. (by a number of excellent people) analyzing the issues that it raises. But I also knew that the DBCFT might have collapsed politically by the time of the talk, and figured that, under that seemingly likely scenario, I'd need a backup plan. This would have the potential, however, to make the talk more fun and interesting for me, by reason of its putting me in a position to contribute more of my own particular thoughts (as opposed to mainly reporting about others' work).

I think we're now at that point. While it's dangerous to base one's ongoing work on assumptions regarding what's going to happen in Washington, it certainly does appear to be the case that the enactment of a destination-based corporate tax is dead in the U.S., at least for the time being.

But it's an interesting question why this thing, which is so different, at least formally, from what everyone else in the world does, should have risen to such prominence before its apparent political collapse. This isn't a criticism of the DBCFT or its proponents - rather, it's a point about the peculiarity of U.S. taxation and tax politics, such that we're the only OECD country without a VAT, our corporate income tax statutory rate is unusually high, etc. It's because things are so peculiar here that the policy aims underlying the proposal took this particular form. And that's worth laying out a bit, in ways that will be more familiar going in to Americans than others, but even for Americans perhaps illuminating to explore.

So here's my current working title: "The Rise and Fall of the DBCFT: What Was That All About?" There might be enough content here to support, not just my talk in Finland on June 1 and short paper in a journal that few Americans will read, but also more extensive U.S. development and dissemination of the main themes.

UPDATE: I've completed slides for the talk, will post them after giving it on June 1, and probably will write a short article version after that.

The DBCFT is of course an interesting topic, and for the above purposes I thought I could reasonably be a consumer at the research stage, and purveyor to my audience in delivering the talk and paper, of the best work that's been done in the U.S. (by a number of excellent people) analyzing the issues that it raises. But I also knew that the DBCFT might have collapsed politically by the time of the talk, and figured that, under that seemingly likely scenario, I'd need a backup plan. This would have the potential, however, to make the talk more fun and interesting for me, by reason of its putting me in a position to contribute more of my own particular thoughts (as opposed to mainly reporting about others' work).

I think we're now at that point. While it's dangerous to base one's ongoing work on assumptions regarding what's going to happen in Washington, it certainly does appear to be the case that the enactment of a destination-based corporate tax is dead in the U.S., at least for the time being.

But it's an interesting question why this thing, which is so different, at least formally, from what everyone else in the world does, should have risen to such prominence before its apparent political collapse. This isn't a criticism of the DBCFT or its proponents - rather, it's a point about the peculiarity of U.S. taxation and tax politics, such that we're the only OECD country without a VAT, our corporate income tax statutory rate is unusually high, etc. It's because things are so peculiar here that the policy aims underlying the proposal took this particular form. And that's worth laying out a bit, in ways that will be more familiar going in to Americans than others, but even for Americans perhaps illuminating to explore.

So here's my current working title: "The Rise and Fall of the DBCFT: What Was That All About?" There might be enough content here to support, not just my talk in Finland on June 1 and short paper in a journal that few Americans will read, but also more extensive U.S. development and dissemination of the main themes.

UPDATE: I've completed slides for the talk, will post them after giving it on June 1, and probably will write a short article version after that.

Thursday, April 27, 2017

2017 Tribeca Film Festival

We've been going for several years now. You get an 8-pack, and that entitles you to 4 films (2 tickets to each). You try to spread them out, one movie every couple of days, reasonable screen times for a working stiff, and pick films that are radically different from each other (as they were this year).

This year's haul: (1) Flower, somewhat dark indie film, adolescent & family dysfunction, 3-1/2 stars out of 4.

(2) Blurred Lines, only 2 to 2-1/2 stars, arts world documentary, too predictable, the basic critique is fine but it ought to have been more original and insightful.

(3) Newton, 3-1/2 stars but possibly our favorite of the group (although Flower was close), drama/comedy from India, sociologically interesting to an Amurrican.

(4) The Circle, 3 stars, liked it but shouldn't have picked it given forthcoming multi-screen commercial release, great atmosphere and good performances by Emma Watson and especially Tom Hanks, (he plays a great quasi-villain, her character as written was a bit incoherent), had some credibility and melodramatic shortcut problems. I haven't read the novel but am curious re. how similar it is or isn't (Eggers did co-author the screenplay).

This year's haul: (1) Flower, somewhat dark indie film, adolescent & family dysfunction, 3-1/2 stars out of 4.

(2) Blurred Lines, only 2 to 2-1/2 stars, arts world documentary, too predictable, the basic critique is fine but it ought to have been more original and insightful.

(3) Newton, 3-1/2 stars but possibly our favorite of the group (although Flower was close), drama/comedy from India, sociologically interesting to an Amurrican.

(4) The Circle, 3 stars, liked it but shouldn't have picked it given forthcoming multi-screen commercial release, great atmosphere and good performances by Emma Watson and especially Tom Hanks, (he plays a great quasi-villain, her character as written was a bit incoherent), had some credibility and melodramatic shortcut problems. I haven't read the novel but am curious re. how similar it is or isn't (Eggers did co-author the screenplay).

Not all 15 percent tax rates are the same

My last post on the 500-word scrawling that has amusingly been called Trump's tax "plan" was quite critical of the proposed 15 percent rate for "business" income, which potentially includes any income that one can contrive to have paid to a business entity (including any state-law entity such as an LLC of which you own 100%), rather than directly to oneself as a wage. I noted that, in practice, this is likely to result in an upside-down rate structure in which rich people commonly pay 15% while their employees pay tax at higher rates. And I noted that it in effect penalizes being an employee who gets paid a salary directly, as if this were a crime that needed to be punished or at least discouraged.

But some readers may have asked: What about the capital gains rate? It was 15% for a while, although it's 20% now. Is the proposed 15% business rate worse than that?

The answer is very clearly Yes. Now, there are some cases in which the 15% capital gains rate works exactly the same way as the "business rate" would - allowing high-earnerrs who have flexibility over cash flow, are well-advised, etc., to get the same result as above. Hedge fund managers can often do this, and it underlies the "carried interest" controversy.

But it's harder to do the capital gains trick than it would be to take advantage of the small business loophole. So less people are able to do it. Plus, there's a whole lot of other stuff mixed in to the capital gains category that has a case for more favorable treatment,

Depending on the particular facts, complicating issues may include the following:

--Capital gain on selling corporate stock gives rise to double taxation if the income is taxed at the corporate level - sometimes a big if.

--There may be nominal inflationary gain mixed in.

--To the extent that capital gain merely reflects earning the normal rate of return on capital, there are arguments for taxing it at a lower rate than that which is economically labor income or rents.

--The capital gains tax is to some extent, and in many cases, a voluntary tax. Hence, the Laffer curve can actually kick in at politically conceivable tax rate levels (e.g., by the time the rate gets into the 30s). This problem is greatly exacerbated by the tax-free step-up in basis for appreciated assets at death, which means the tax can be permanently avoided, rather than merely being deferred. That rule ought to be fixed, but as long as it isn't it constrains how high the capital gains rate should be.

This is not necessarily to defend a 15% or even 20% capital gains rate, especially if we have options at hand beyond just raising the rate, designed (for example) to reduce the feasibility of shoving labor income into the capital gains basket.

But at least we are in the realm of complicated issues and policy tradeoffs - which is not the case with respect to a general 15% "business rate."

It's true that, if we enact a significantly lower corporate rate, it's important to think about the corporate versus non-corporate business tax rate relationship. But (a) the corporate tax is to a degree, albeit imperfectly, more about globally mobile capital than the "business tax," (b) the response should focus on limiting use of the corporation as a tax shelter to escape individual rates on labor income and rents - not extending this problem even further, and (c) corporate income still potentially faces shareholder-level taxation, via the taxation of capital gain and dividends.

Great example of how the "business rate" works: Kansas has idiotically, and to its great detriment, enacted a version of what Trump now wants to do. The Kansas rules actually exempt so-called business income, since state rates are much lower than federal to begin with.

In response, Bill Self, the coach of the Kansas University basketball team, who gets paid $3 million per year, restructured a bit so that 90% of his salary would be "business income' that was exempt from the Kansas income tax. Gruesome details here.

Enacting the 15% business rate, especially in light of Trump's personal stake in the matter (so far as we can understand it despite the lack of transparency), and in light of the Kansas experience, would be straight-out looting and fiscal sabotage, not a policy move that is reasonably debatable or defensible.

But some readers may have asked: What about the capital gains rate? It was 15% for a while, although it's 20% now. Is the proposed 15% business rate worse than that?

The answer is very clearly Yes. Now, there are some cases in which the 15% capital gains rate works exactly the same way as the "business rate" would - allowing high-earnerrs who have flexibility over cash flow, are well-advised, etc., to get the same result as above. Hedge fund managers can often do this, and it underlies the "carried interest" controversy.

But it's harder to do the capital gains trick than it would be to take advantage of the small business loophole. So less people are able to do it. Plus, there's a whole lot of other stuff mixed in to the capital gains category that has a case for more favorable treatment,

Depending on the particular facts, complicating issues may include the following:

--Capital gain on selling corporate stock gives rise to double taxation if the income is taxed at the corporate level - sometimes a big if.

--There may be nominal inflationary gain mixed in.

--To the extent that capital gain merely reflects earning the normal rate of return on capital, there are arguments for taxing it at a lower rate than that which is economically labor income or rents.

--The capital gains tax is to some extent, and in many cases, a voluntary tax. Hence, the Laffer curve can actually kick in at politically conceivable tax rate levels (e.g., by the time the rate gets into the 30s). This problem is greatly exacerbated by the tax-free step-up in basis for appreciated assets at death, which means the tax can be permanently avoided, rather than merely being deferred. That rule ought to be fixed, but as long as it isn't it constrains how high the capital gains rate should be.

This is not necessarily to defend a 15% or even 20% capital gains rate, especially if we have options at hand beyond just raising the rate, designed (for example) to reduce the feasibility of shoving labor income into the capital gains basket.

But at least we are in the realm of complicated issues and policy tradeoffs - which is not the case with respect to a general 15% "business rate."

It's true that, if we enact a significantly lower corporate rate, it's important to think about the corporate versus non-corporate business tax rate relationship. But (a) the corporate tax is to a degree, albeit imperfectly, more about globally mobile capital than the "business tax," (b) the response should focus on limiting use of the corporation as a tax shelter to escape individual rates on labor income and rents - not extending this problem even further, and (c) corporate income still potentially faces shareholder-level taxation, via the taxation of capital gain and dividends.

Great example of how the "business rate" works: Kansas has idiotically, and to its great detriment, enacted a version of what Trump now wants to do. The Kansas rules actually exempt so-called business income, since state rates are much lower than federal to begin with.

In response, Bill Self, the coach of the Kansas University basketball team, who gets paid $3 million per year, restructured a bit so that 90% of his salary would be "business income' that was exempt from the Kansas income tax. Gruesome details here.

Enacting the 15% business rate, especially in light of Trump's personal stake in the matter (so far as we can understand it despite the lack of transparency), and in light of the Kansas experience, would be straight-out looting and fiscal sabotage, not a policy move that is reasonably debatable or defensible.

Wednesday, April 26, 2017

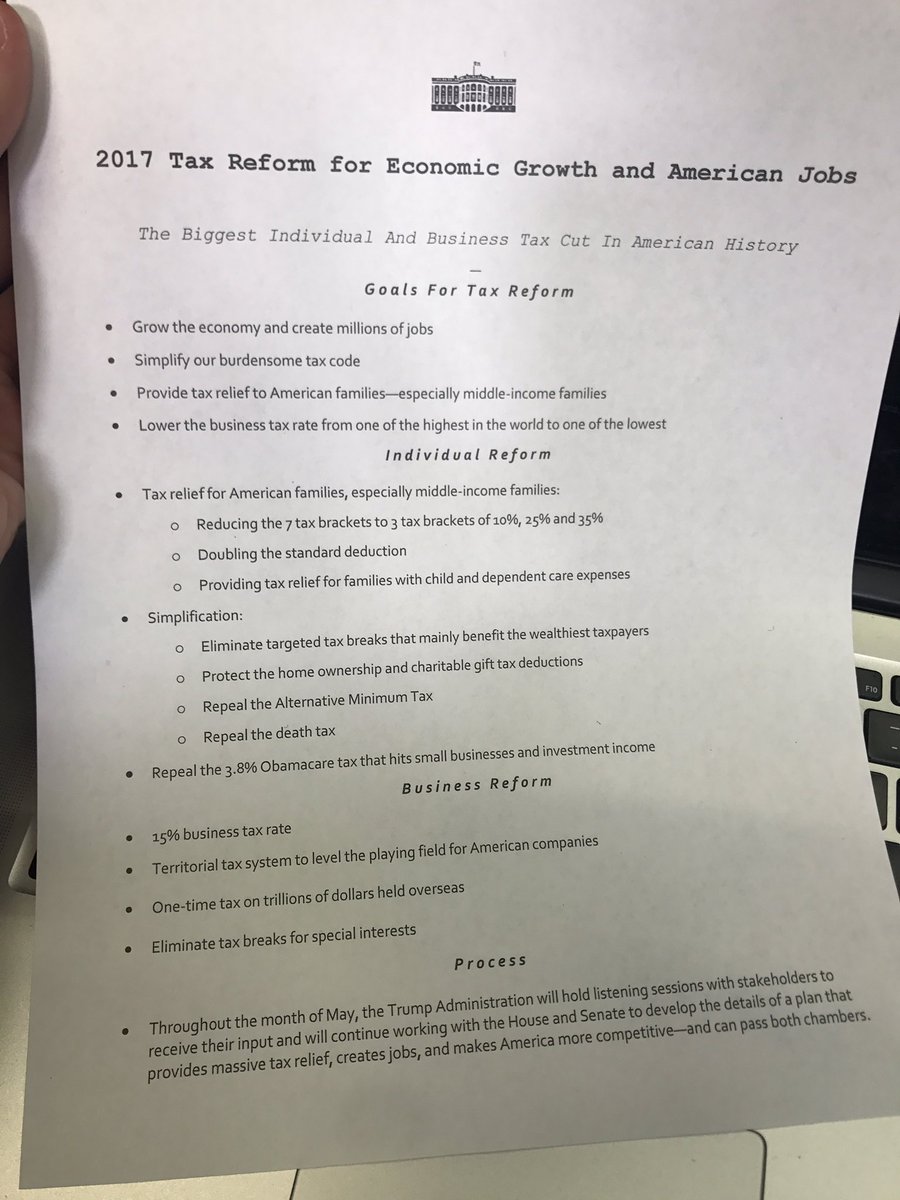

Preliminary thoughts on the Trump Administration's tax "plan" - what's the rationale for an "employee surtax"?

Perhaps the Trump tax proposal shouldn't be taken too seriously, as it's apparently being rushed out to meet the self-imposed "100 days" deadline and may face mixed prospects at best on the Hill. But when an administration actually claims it wants to do something, it can't just be laughed at as non-serious, even if the proposal is in fact a joke substantively. After all, they're showing us who they are. And what's more, who knows what might end up happening?

That said, suppose the Trump plan includes a 15% rate for corporations and "small business," defined as all passthroughs as well as proprietorships - i.e., non-employee business and labor income generally. And suppose there are neither serious revenue offsets nor significant efforts to limit tax planning that takes advantage of the disparity between the twin 15% rates and the higher (up to 33%?) rates that would still apply to individuals.

Point 1, this seems likely to be such a huge revenue loser that the growth effects might be negative, given fiscal drag from the extra deficits and debt.

Point 2, the Trump tax plan brings to mind the gabelle - the infamous French salt tax, from before the French Revolution, from which nobles were exempt. Given the degree of correlation between income levels and likely ability to take advantage of the 15% passthrough/small business/non-employee rate, it would frequently apply higher marginal rates to people at modest income levels than to those at high income levels.

Think of a law firm in which the partners pay tax at a 15% rate, while the associates, paralegals, and secretaries pay at higher rates (up to 35%). Or think of a high-priced surgeon who pays tax at a 15% rate, while the secretary who answers his phone might pay tax at a higher rate.

The reason I analogize it to the gabelle, rather than just saying the rate structure is upside down, is because one could conceptualize it as being equivalent to having a generally applicable 15% rate, plus (once the marginal rate for employment income gets above that level) a special surtax or penalty tax that applies only to employees, and thus effectively fines or punishes people for having this status. The self-employed, like pre-revolutionary France's nobles when they used salt, are exempt from the employee surtax.

True, entitlement to the lower rate is not perfectly reverse income-correlated. Uber drivers would presumably get the 15% rate. And high-paid CEOs, to the extent they were getting cash salary, would presumably reach the 33% marginal rate. But the "employee surtax" of up to 20% is one from which proportionately more "nobles" than "commoners" would be exempt.

Depending on how the plan defines non-employee income, I suppose it's possible that law professors could start claiming the 15% rate as to their Schedule C income, such as from consulting. So there's that.

Point 3. Why have an employee surtax? This is not only regressive, but inefficient. It interferes with people's making normal business arrangements on a pretax basis. It creates a large tax penalty for employment, as opposed to other ways of earning labor income. Apart from the pure tax planning aspects of trying to avoid employment status, it could shift actual business arrangements in wasteful directions. Indeed, if employment status is tax-penalized enough, I wonder if the incidence could start to shift a bit. This is the scenario in which employee wages have to rise, pre-tax, in order to make up for the tax penalty. It's municipal bonds in reverse - they generally offer less pre-tax than, say, corporate bonds because the income is exempt. In this scenario, employees would be getting more pre-tax than the self-employed / independent contractors because they were in effect subject to a special "employee surtax."

That said, suppose the Trump plan includes a 15% rate for corporations and "small business," defined as all passthroughs as well as proprietorships - i.e., non-employee business and labor income generally. And suppose there are neither serious revenue offsets nor significant efforts to limit tax planning that takes advantage of the disparity between the twin 15% rates and the higher (up to 33%?) rates that would still apply to individuals.

Point 1, this seems likely to be such a huge revenue loser that the growth effects might be negative, given fiscal drag from the extra deficits and debt.

Point 2, the Trump tax plan brings to mind the gabelle - the infamous French salt tax, from before the French Revolution, from which nobles were exempt. Given the degree of correlation between income levels and likely ability to take advantage of the 15% passthrough/small business/non-employee rate, it would frequently apply higher marginal rates to people at modest income levels than to those at high income levels.

Think of a law firm in which the partners pay tax at a 15% rate, while the associates, paralegals, and secretaries pay at higher rates (up to 35%). Or think of a high-priced surgeon who pays tax at a 15% rate, while the secretary who answers his phone might pay tax at a higher rate.

The reason I analogize it to the gabelle, rather than just saying the rate structure is upside down, is because one could conceptualize it as being equivalent to having a generally applicable 15% rate, plus (once the marginal rate for employment income gets above that level) a special surtax or penalty tax that applies only to employees, and thus effectively fines or punishes people for having this status. The self-employed, like pre-revolutionary France's nobles when they used salt, are exempt from the employee surtax.

True, entitlement to the lower rate is not perfectly reverse income-correlated. Uber drivers would presumably get the 15% rate. And high-paid CEOs, to the extent they were getting cash salary, would presumably reach the 33% marginal rate. But the "employee surtax" of up to 20% is one from which proportionately more "nobles" than "commoners" would be exempt.

Depending on how the plan defines non-employee income, I suppose it's possible that law professors could start claiming the 15% rate as to their Schedule C income, such as from consulting. So there's that.

Point 3. Why have an employee surtax? This is not only regressive, but inefficient. It interferes with people's making normal business arrangements on a pretax basis. It creates a large tax penalty for employment, as opposed to other ways of earning labor income. Apart from the pure tax planning aspects of trying to avoid employment status, it could shift actual business arrangements in wasteful directions. Indeed, if employment status is tax-penalized enough, I wonder if the incidence could start to shift a bit. This is the scenario in which employee wages have to rise, pre-tax, in order to make up for the tax penalty. It's municipal bonds in reverse - they generally offer less pre-tax than, say, corporate bonds because the income is exempt. In this scenario, employees would be getting more pre-tax than the self-employed / independent contractors because they were in effect subject to a special "employee surtax."

Tuesday, April 25, 2017

NYU Tax Policy Colloquium, week 13: Joel Slemrod (et al), "Taxing Hidden Wealth"

Yesterday our colloquium speaker was Joel Slemrod, presenting "Taxing Hidden Wealth: The Consequences of U.S. Enforcement Initatives on Evasive Foreign Accounts."

The paper uses IRS data to examine what happened after (and presumably in consequence of) a number of steps being taken to address U.S. individual income tax evasion via the hiding of income in foreign accounts. The relevant changes during the period being studied included (1) persuading a number of tax havens to accept information exchange agreements, (2) ending Swiss bank secrecy in the aftermath of the UBS scandal, (3) increasing penalties and enforcement with respect to non-filing of legally mandated FBAR foreign financial asset and bank account disclosures, (4) enacting and implementing FATCA, and (5) offering voluntary disclosure programs under which individuals who had failed to report foreign income could step forward and avoid criminal penalties (although they would have to pay several years' back taxes plus interest and 20% to 27.5% penalties).

One cannot in the abstract predict how effective such measures will be. For example, they might simply induce people to do a better job of hiding their foreign accounts. But the paper finds that compliant responses were quite large, leading to significant increases in tax revenue and reported foreign source interest, dividends, and capital gains. So the set of initiatives appears to have been quite successful, coming closer to what an optimist than a pessimist might have expected up front.

The paper also finds that there were significant "quiet disclosures." That is, people suddenly started filing FBAR reports and including lots of foreign interest and dividend income on their tax returns, as if all this had suddenly arisen in Year 1 of such reporting and inclusion. It's a fair inference that this commonly involved switching from evasion to compliance without participating in the voluntary disclosure programs. This had the advantage of permitting the quiet disclosers to avoid paying back taxes et al, at the cost of leaving them potentially subject to an audit that could include a criminal tax fraud investigation. The IRS warned people that quiet disclosure was a bad idea given this potential blowback, but in practice appears not, at least so far, to have followed up significantly on the threat.

The size and clarity of the empirical results promise this paper major (and well-deserved) attention. For example, if FATCA repeal starts being discussed, there's strong evidence here that the full panoply of what has been done (including but not limited FATCA) has worked very well.

Also of interest is the size of the offshore accounts that were newly reported by U.S. taxpayers in the aftermath of the suite of new policies. The paper estimates that more than 90% of the newly reported foreign asset values came from accounts worth more than $1 million or more. So these were not small fish by most lights.

Two things that one would like to know more about, and that further work by the authors might be able to help illuminate, are:

(1) How rich are these million-dollar account-holders? Contrast the case of (a) a super-rich individual who shoves a million-plus into foreign accounts, while holding other wealth more transparently, from that of (b) someone whose business, after several decades, sells for a million-dollar profit that gets stashed in a foreign account. So here it's the big enchilada in this individual's portfolio, and he or she, while evidently successful, is not super-rich. One reason that this is of interest is that, insofar as (a) is a common answer, it would tend to undermine the standard assumption that the super-rich mainly just avoid taxes, rather than evade them.

(2) Insofar as foreign accounts were being used to evade U.S. taxes, was it mainly about the principal, or just the interest? If principal, then the full amount deposited in the accounts should have been taxed (whether as capital gain, such as from selling a business, or ordinary income, such as contractor fees) but wasn't. But less was at stake (albeit, still raising an important enforcement issue) if people were just hiding the interest and dividends, etc., that they earned on previously earned after-tax income.

People who took advantage of the voluntary disclosure programs got a really good deal insofar as they were able to hide the principal and wait until enough years have passed so the lookback wouldn't find it.

The paper uses IRS data to examine what happened after (and presumably in consequence of) a number of steps being taken to address U.S. individual income tax evasion via the hiding of income in foreign accounts. The relevant changes during the period being studied included (1) persuading a number of tax havens to accept information exchange agreements, (2) ending Swiss bank secrecy in the aftermath of the UBS scandal, (3) increasing penalties and enforcement with respect to non-filing of legally mandated FBAR foreign financial asset and bank account disclosures, (4) enacting and implementing FATCA, and (5) offering voluntary disclosure programs under which individuals who had failed to report foreign income could step forward and avoid criminal penalties (although they would have to pay several years' back taxes plus interest and 20% to 27.5% penalties).

One cannot in the abstract predict how effective such measures will be. For example, they might simply induce people to do a better job of hiding their foreign accounts. But the paper finds that compliant responses were quite large, leading to significant increases in tax revenue and reported foreign source interest, dividends, and capital gains. So the set of initiatives appears to have been quite successful, coming closer to what an optimist than a pessimist might have expected up front.

The paper also finds that there were significant "quiet disclosures." That is, people suddenly started filing FBAR reports and including lots of foreign interest and dividend income on their tax returns, as if all this had suddenly arisen in Year 1 of such reporting and inclusion. It's a fair inference that this commonly involved switching from evasion to compliance without participating in the voluntary disclosure programs. This had the advantage of permitting the quiet disclosers to avoid paying back taxes et al, at the cost of leaving them potentially subject to an audit that could include a criminal tax fraud investigation. The IRS warned people that quiet disclosure was a bad idea given this potential blowback, but in practice appears not, at least so far, to have followed up significantly on the threat.

The size and clarity of the empirical results promise this paper major (and well-deserved) attention. For example, if FATCA repeal starts being discussed, there's strong evidence here that the full panoply of what has been done (including but not limited FATCA) has worked very well.

Also of interest is the size of the offshore accounts that were newly reported by U.S. taxpayers in the aftermath of the suite of new policies. The paper estimates that more than 90% of the newly reported foreign asset values came from accounts worth more than $1 million or more. So these were not small fish by most lights.

Two things that one would like to know more about, and that further work by the authors might be able to help illuminate, are:

(1) How rich are these million-dollar account-holders? Contrast the case of (a) a super-rich individual who shoves a million-plus into foreign accounts, while holding other wealth more transparently, from that of (b) someone whose business, after several decades, sells for a million-dollar profit that gets stashed in a foreign account. So here it's the big enchilada in this individual's portfolio, and he or she, while evidently successful, is not super-rich. One reason that this is of interest is that, insofar as (a) is a common answer, it would tend to undermine the standard assumption that the super-rich mainly just avoid taxes, rather than evade them.

(2) Insofar as foreign accounts were being used to evade U.S. taxes, was it mainly about the principal, or just the interest? If principal, then the full amount deposited in the accounts should have been taxed (whether as capital gain, such as from selling a business, or ordinary income, such as contractor fees) but wasn't. But less was at stake (albeit, still raising an important enforcement issue) if people were just hiding the interest and dividends, etc., that they earned on previously earned after-tax income.

People who took advantage of the voluntary disclosure programs got a really good deal insofar as they were able to hide the principal and wait until enough years have passed so the lookback wouldn't find it.

Wednesday, April 19, 2017

Libertarianism and support for progressive redistribution

In light of this past Monday's paper at our colloquium discussing the possibility that libertarians might support a universal basic income, I thought it might be germane to note my 2013 article, "The Forgotten Henry Simons," which explains how and why Simons combined (a) considering himself a libertarian, at a time when this was a far lonelier stance than it is today, with (b) favoring a highly progressive income tax.

The accepted meaning of "libertarianism" has changed significantly since Simons died more than 70 years ago, but he was indeed closely associated with Friedrich Hayek, and George Stiglitz dubbed him the "Crown Prince of ... the Chicago school of economics."

The accepted meaning of "libertarianism" has changed significantly since Simons died more than 70 years ago, but he was indeed closely associated with Friedrich Hayek, and George Stiglitz dubbed him the "Crown Prince of ... the Chicago school of economics."

Recent interview on corporate tax reform and border adjustment

A few weeks back I was interviewed (via email) by Yossi Krausz, the managing editor of Ami Magazine, for an article on the prospects for tax reform. They're an NYC magazine aimed mainly at the Orthodox Jewish community. It was an Ami reporter who, back in February, asked Trump the question about rising anti-Semitism around the country that drew an angry and thin-skinned response from him.

The article has now appeared, although it doesn't appear to be available online. Title: "Will Trump Pass Tax Reform? Doubts in the Wake of the Healthcare Debacle." Here are the quotes from my interview:

1) I called it unlikely that the Democrats would cooperate with the Republicans on a corporate tax reform bill: "Many Democrats want to lower the corporate rate, and they may also share Republican dislike for (universally reviled!) aspects of our current systm for taxing US multinationals' foreign source income, but I doubt that the parties will find common ground."

2) Re. the border adjustment tax: "I expect it to be dropped due to intense opposition in some circles, plus the difficulty of making it work right, which would require more expertise and time than the White House or congressional leadership is williug or able to bring to bear on it....

"Almost no one understands border adjustment. This leads to both undue support and undue opposition; for example, people who like tariffs may support it although it's trade-neutral over the long run, people who hate value-added taxes may support it even though it's basically a VAT plus a couple of extra features, and companies that think it will hurt them may be wrong about the economics (although we don't know this for sure)."

The article has now appeared, although it doesn't appear to be available online. Title: "Will Trump Pass Tax Reform? Doubts in the Wake of the Healthcare Debacle." Here are the quotes from my interview:

1) I called it unlikely that the Democrats would cooperate with the Republicans on a corporate tax reform bill: "Many Democrats want to lower the corporate rate, and they may also share Republican dislike for (universally reviled!) aspects of our current systm for taxing US multinationals' foreign source income, but I doubt that the parties will find common ground."

2) Re. the border adjustment tax: "I expect it to be dropped due to intense opposition in some circles, plus the difficulty of making it work right, which would require more expertise and time than the White House or congressional leadership is williug or able to bring to bear on it....

"Almost no one understands border adjustment. This leads to both undue support and undue opposition; for example, people who like tariffs may support it although it's trade-neutral over the long run, people who hate value-added taxes may support it even though it's basically a VAT plus a couple of extra features, and companies that think it will hurt them may be wrong about the economics (although we don't know this for sure)."

Tuesday, April 18, 2017

Tax policy colloquium, week 12: Miranda Perry Fleischer's "Atlas Nods: The Libertarian Case for a Basic Income" - Part 2

My prior post touched

on a variety of background philosophical issues raised by Miranda Perry Fleischer’s

presentation yesterday at the colloquium of her paper (co-authored with Daniel

Hemel), Atlas Nods: The Libertarian Case

for a Basic Income. Herewith are some brief reflections on what I consider

issue 2: how a demogrant or “universal basic income” (UBI) might be designed.

One important general point is that, while people often think about UBI in very

basic terms – i.e., as just a uniform cash grant – its optimal design raises

many of the same issues as designing, say, income-conditioned transfers or

income tax rate brackets. For example:

1) Cash vs. non-cash – As noted in

the prior post, David Bradford and I wrote about this set of issues some 18

years ago. Despite the consumer sovereignty arguments for giving poor people cash

rather than in-kind benefits, the grounds for in-kind are not limited to

paternalism. For example, even apart from altruistic externalities (as in the

case where the altruist would rather give people food or shelter than items

that they reasonably preferred), the need for in-kind benefits may respond to

other market failures, as arguably in healthcare and health insurance, or may

reflect distributive desert (e.g., as evidence of a poor health endowment.

Issues of cash

versus non-cash are not limited to what we may think of as in-kind transfers,

but also extend to the provision of goods and services that do not have a

purely public goods (i.e., non-rival and non-excludable) character. One could

imagine a classical liberal proposing, first, that public schools be replaced

by vouchers for private schools, and then, second, that the vouchers be

replaced by straight-up cash. But this would obviously be subject to objection.

housing,

healthcare, public schools – once allow altruistic externalities, a lot of

stuff! Especially

2) Which programs should one trade in for the UBI? – On both the

right and the left, views about the UBI often are influenced (either expressly

or implicitly) by the view that its adoption might either increase or reduce

the overall amount of redistribution through fiscal and other policy. While such

effects might certainly be relevant to the evaluation, it is also desirable to

think about it, purely as a design matter, from a broadly distribution-neutral

standpoint. Hence, as in the paper by Perry Fleischer and Hemel, it is worth asking

which government programs might be traded in for the UBI if it were adopted.

This is made

more complicated, however, by the fact that various programs combine a

vertically redistributive element with addressing issues that are distinct from

just poverty. For example, unemployment

insurance is not just about being poor because one lost one’s job, but about

negative income shocks that may adversely affect people. Social Security has

significant distributional effects but is also a mechanism for putting a floor

on one’s retirement saving (taken as given one’s lifetime income, net of taxes

and transfers).

3) Who should get the UBI? – Here the

issues include those around legal and undocumented immigration, residence,

etcetera.

4) Age of the recipient – Should babies

and young children, via the custodial parents or other caretakers, immediately

get the same full amount as adults? Does it matter that their current consumption

needs might be lower? Would this affect decisions about having children or

about custody, and if so what do we think of these effects? Should seniors get

larger annual grants than working-age adults, because they are more likely to

be unable to work? (This question would intersect with those of Social Security

and Medicare design.)

5) Other tax/transfer design issues – Should

household structure matter? (E.g., couples versus singles.) One can’t just

assume not, given the complexity of the issues here. Should there be regional

cost-of-living adjustments?

6) Conditional vs. unconditional – The UBI is

neither income-conditioned nor conditioned on willingness to work. The former

is just optics, but the latter is important (albeit, not limited to UBI; one

can have the same issue with expressly income-conditioned welfare benefits).

The reason that

it’s just optics not to income-condition the UBI is that limiting it based on

income is just another way of applying an effective marginal tax rate. For

example, suppose that Assyria has a $10,000 demogrant, along with a 50% tax

rate on one’s first $20,000 of income (not counting the demogrant), whereas

Babylonia has a 0% tax rate on the first $20,000 of income, but also provides

$10,000 in “welfare benefits” to people with zero income, ratably reduced to

zero in welfare benefits as income increases from 0 to $20,000. No matter what

your income level, you’ll end up with the same net benefit in either society.

So it is only true optically, not substantively, that Assyria is giving the

cash transfer even to its rich people (who presumably don’t need it), whereas

Babylonia isn’t.

Work

conditioning does matter substantively, however, whether or not the grant for

poor people is expressly income-conditioned. And here, getting back to issues

from my prior post regarding whether libertarians or classical liberals should

like the UBI, things get trickier. If you have the Eric Mack view that rescue

should only extend to those who are faultless, a willingness-to-work

requirement may make sense. Indeed, even within a utilitarian framework there

are arguments for it, although here they would be purely consequentialist.

(These might pertain, for example, to positive externalities or internalities

associated with requiring people to work if they can.)

Fleischer-Perry

and Hemel challenge the case for a work requirement, under a libertarian or

classical liberal framework, by arguing that in practice it is likely to be

unacceptably intrusive and error-prone. But arguably that puts it a bit strongly,

if the filter is not completely ineffectual and there are other reasons for

favoring it.

7) A single up-front grant versus periodic (such as

annual or monthly) grants – Fleischer Perry and Hemel rightly

note that a “luck egalitarian” might dislike the fact that, with periodic UBI

payments, the longer-lived end up getting more money than the

shorter-lived. Life annuities (as under

Social Security) would appear to be anti-insurance if one were thinking purely

in terms of overall lifetime welfare. That is, if you’re already luckier in

that you get to live longer, you’re made luckier still by getting more money

too. What makes a life annuity true insurance, rather than anti-insurance, is

that living longer creates the risk that one will need more resources for one’s

support. So it increases expected utility despite its rewarding those who are

(in an overall rather than a marginal utility sense) already the “winners.”

With incomplete

capital markets, the choice between an upfront grant and periodic grants

matters for reasons apart from variations in life expectancy and actual

lifespan. Ackerman and Alstott note that, if it’s hard to borrow against the

value of expected future grants, cash upfront may be more empowering in some

circumstances. (Of course, there are other mechanisms for addressing this,

e.g., education loans and not currently taxing expected future earnings.) But

on the other hand the empowerment might also lead to costly errors in judgment

while one is still young. Arguably libertarians, because of the not- just-instrumental

value they place on choice (including any notion that it’s just your tough luck

if you suffer from choosing poorly), should be more sympathetic than others to

allowing people, say, to pledge future UBI in exchange for cash today.

8) Is the UBI “too popular,” from a libertarian or

classical liberal standpoint? – Fleischer-Perry and Hemel question

the premise by some that libertarians and classical liberals who dislike

redistribution, but figure that there is bound to be some of it, should like

the UBI as a kind of political second-best, limiting the amount of redistribution

and the related intrusion into people’s lives. They base this part on the idea

that “universal” programs can become very popular. A case in point is the

decision by Social Security’s founders to call it a “universal” program (and to

make its transfers between participants relatively opaque). But there is little

evidence to date of the risk that it would become, at least from a particular

standpoint, too popular. (BTW, I note also that some on the left are skeptical

of UBI because they believe it would cause the government’s redistributive mechanisms

to end up being smaller, rather than larger.) The two main things that seem to

limit UBI’s political appeal are (a) fiscal illusion from its not being expressly

income-conditioned (as in, “Why give it to Bill Gates?”, and more substantively

(b) notions of more limited distributive desert that are related to

conditionality and willingness to work.

Tax policy colloquium, week 12: Miranda Perry Fleischer's "Atlas Nods: The Libertarian Case for a Basic Income" - Part 1

Yesterday at the colloquium, Miranda Perry Fleischer presented the

above-titled paper (coauthored by Daniel Hemel). They posit that libertarianism

(which they note has multiple strands) and classical liberalism might be

consistent with favoring limited redistribution in the form of a safety net

protecting the poor, and that this might plausibly take the form of supporting a

universal basic income (UBI) or demogrant.

Three great things about the paper and the project are (1) it reminds us

that there are more versions of libertarianism (and affiliated sentiments) out

there than just Nozick, (2) it addresses real world policy issues based on a

normative framework different from the usual one (or mine), thereby expanding

the breadth of discourse, and (3) UBI / demogrants is a great topic, even if

one doesn’t consider it currently politically practical. Like the long-running income tax vs.

consumption tax debate in U.S. tax policy circles, it doesn’t just illuminate a

particular instrument choice but is a well-suited vehicle for exploring

fundamental underlying issues.

BTW, I’ve written in the past about varieties of libertarianism in

relation to the very interesting case of Henry Simons, and about demogrants vs.expressly income-conditioned “welfare,” and (with David Bradford) about cashversus non-cash benefits. So this is

territory that I like and have thought about before (albeit not extremely

recently).

My thoughts about the paper and the topic are best divided into two

headings: using libertarianism to assess the UBI, and UBI design issues. I’ll

discuss Part 1 in this blog post, and Part 2 in a follow-up.

1. Using libertarianism to assess the UBI

Given the if-then structure of the paper’s analysis – “If you subscribe

to some version of libertarianism or classical liberalism, then you might favor

a UBI” – debating the merits of those views is not the most pertinent way to

respond. But because one needs to

understand the rationales in order to apply different versions of these

doctrines, I find it hard to stay away entirely from raising issues that may

reflect my skepticism.

1) Hypothetical

consent – In general, this family of normative views requires consent in

order for people to be subject to limitations on their property rights (if

those meet the Lockean, etc. tests for validity). But it can be hypothetical

consent that a reasonable person would have to grant.

Sometimes these

exercises might involve comparing the actual state of affairs to a version of

the state of nature, or to a world in which the state doesn’t exist (but that’s

otherwise the same?) or in which property rights don’t exist, or perhaps

something else. I admittedly find myself unclear for the rationale for picking

a particular counterfactual, which might be a quite fanciful and artificial

construct. I’m also inclined to base my own preferred hypothetical consent

exercise on Harsanyi’s behind-the-veil analysis, where all you don’t know is

which person you are – a device for valuing people’s welfare equally – and which

can push one towards utilitarianism based on an expected-utility analysis.

2) How

decide the relevance of empirical inputs? – The paper extensively discusses

various empirical issues, as it should given their relevance. But given the deontological foundations of at

least some versions of libertarianism, it’s hard to reach firm conclusions

about how they would affect the analysis.

For example, the paper notes evidence in support of the view that, if

poor people were given cash in lieu of in-kind benefits (e.g., Food Stamps or

housing subsidies), they might tend to use the money wisely rather than

foolishly. This might be normatively irrelevant, however, under a view in which

people should be given maximum freedom of choice but if they screw it up that

is purely on them.

3) Should

people be rescued from the consequences of their own mistakes? – Suppose X

is poor because X made bad choices. Should government policy help X out? Under

utilitarianism, the principle of beneficence – from counting everyone’s welfare

positively – says yes. There may be a tradeoff in practice, because rescuing

people from the consequences of costly mistakes reduces their incentive to

avoid incurring the costs of those mistakes, but the utility gain to X is

counted no differently than if there had been no mistake made.

Libertarians

often care about (and moralize) choice for its own sake, rather than just

instrumentally. A consequence is that it might matter why someone is poor – due

to bad choices, or circumstances beyond her control – even without regard to

the empirical significance of incentive effects. In this regard, a well-known hypothetical by

the philosopher Eric Mack plays an important role in the paper’s analysis. http://murphy.tulane.edu/people/eric-mack

As paraphrased

by Perry Fleischer and Hemel, Mack ““ask[s] us to imagine a fully-prepared hiker

on a well-planned excursion. Through no fault of her own, she encounters

unpredicted fatally cold temperatures. The hiker comes across a locked but

unoccupied cabin in the woods whose shelter, fire, and blankets would save her

life. Entering the cabin to save her life, however, would violate the owner’s

property rights. Yet according to Mack,

the ‘most basic intuition’ is that ‘no plausible moral theory’ would require the

faultless hiker to freeze to death. ‘Even more clearly,’ Mack writes, ‘no moral

theory that builds upon the separate value of each person’s life and well-being

can hold that Freezing Hiker is morally bound to grin and bear it.’ For these

reasons, Mack believes that libertarianism must tolerate some violation of

private property rights—at least in the extreme circumstances of the freezing

hiker.” However, “[o]nly instances of

extreme need … justify violating the owner’s property rights in Mack’s view. If

our hiker were simply tired and sore (and not in fatal peril), no violation

would be justified.”

One question I

have here is: What does it mean to say that the hiker was fully-prepared and

excursion unplanned, yet that, through no fault of her own, she encountered

unpredicted fatally cold temperatures? Evidently, there was not, ex ante, a

zero percent chance that this would happen. She deliberately took the risk that

it would happen by going on the hike, instead of staying home, and not

equipping herself with sufficient protective garb for this eventuality. So we

presumably are in the realm of evaluating the reasonableness of her

precautions, as a function of the likelihood that there would be so severe a

cold snap and the costliness of being ready for it.

I myself would

want the hiker to be aided even if she planned poorly, and even if she merely

faced extreme discomfort, rather than death. Whether I’d want to impose the

cost of helping her on the cabin owner, which would affect that individual’s

incentive to maintain an intact and well-stocked cabin in the woods despite

being less than eager to have invaders take advantage of it, would depend on

evaluating the costs and benefits, rather than being decided on the basis of abstract

reasoning about property rights. But one broader issue I have with the style of

reasoning reflects my sense that it contains discontinuities that I find intuitively

unappealing. E.g., certain death between lesser degrees of harm; planning that

meets the cost-benefit test (or whatever we use to determine whether the hiker

was at fault) versus that which falls just short.

Mack offers a

rationale, within libertarianism, for favoring some degree of safety net

protection for the poor. But the relevance he ascribes to lack of fault, and the

extremity of the harm that the hypothetical posits, might tend to weigh against

using his argument to support a UBI. Perry Fleischer and Hemel argue, however,

that any such negative implication for the UBI can be overcome, e.g., by reason

of mistakes that the government might make in seeking to assess fault.

4) Sufficientarianism

and discontinuity – Other discussion in the paper notes that some

self-described libertarians or classical liberals support a “sufficientarian”

safety net, so that everyone is guaranteed a minimum level of resources even though

inequality is not otherwise a relevant social policy concern. The journey from this view to supporting a

UBI is certainly a lot more straightforward than that from wanting to help only

people who are faultless. Once again I find its discontinuity intuitively

uncongenial. Put in my sort of terms, it posits a marginal social value to

increasing someone’s welfare that is high until the recipient of the benefit

reaches “sufficiency,” at which point the social value of further increases in

welfare drops to zero. And “sufficiency” presumably isn’t just a matter of

staying alive, but of being able to function at some level of adequacy; it also

presumably would be higher in the U.S. in 2017 than 1717, or for that matter

anywhere in 2017 BC.

5) What

sorts of market failures are relevant to government policy? – While libertarians

and classical liberals like market outcomes at least in part for underlying

philosophical reasons, pertaining to their particular views about property

rights, voluntariness and consent, etc., a utilitarian also will like markets

if sympathetic to mainstream economic analysis – subject, however, to believing

that the preconditions for markets to work well are sufficiently met. (NoahSmith and others, however, use the term “101ism” or “Econ 101ism” to describe

what they regard as undue optimism regarding the frequency with which these

preconditions are met in practice.)

Many

self-styled libertarians or classical liberals accept, however, not just that

market failure can occur, but also that its occurrence may justify government

intervention. An example would be using compulsory taxation to fund important

public goods that markets would fail to provide due to the free rider problem

(arising from the public goods’ nonexcludability). Pigovian taxation to address negative

externalities such as pollution (if transaction costs impede just relying on

the assignment of property rights) is a second example.

Once one starts

down this road, however, one can go pretty far. For example, full-out

redistributive taxes and transfers can be rationalized as providing insurance

against ability risk (and undiversified human capital risk given the need to

specialize) that private markets would

provide if not for the adverse selection problem, which governments, unlike

private insurance companies, can address by mandating participation. (There is

still a moral hazard problem, which governments are stuck with, but they presumably

don’t reduce the optimal insurance coverage to zero.)

I’m not clear

on how (or how persuasively) one can stave off this line of argument once one

has accepted that market failure can make a case for government intervention. Merely

being skeptical about the social benefits to be derived in practice from

following such a policy can convert the dispute from a purely philosophical one

into one with significant empirical content (and potentially within a

utilitarian or other welfarist framework).

This can

complicate evaluating how a generally pro-market classic liberal who is open to

consequentialist arguments based on empirical evidence ought to respond to the

case for a more broadly redistributive fiscal system. But a further question about

market failure’s significance to the analysis is raised by the paper’s quoting

Milton Friedman (who advocated “negative income taxation” that is effectively

the same as having a UBI) as follows: “I am distressed by the sight of poverty;

I am benefited by its alleviation; but I am benefited equally whether I or

someone else pays for its alleviation . . . . To put it

differently, we might all of us be willing to contribute to the relief of

poverty, provided everyone else did.

We might not be willing to contribute to the same amount without such

assurance.” Hence, if voluntariness falls short we may have the standard public

goods rationale for supplying poverty relief by government mandate.

A utilitarian

would certainly be inclined to agree that the altruistic externality cited by

Friedman – in that X’s poverty hurts the observer, not just X – is at least

presumptively relevant to policy. But it does open a can of worms, for both

Friedman and utilitarians. E.g., what if only one minds the poverty of people

in one’s own ethnic group? Or observer preferences that are either

anti-redistributive or affirmatively malevolent towards others? What if the way

in which one wants to help another person reflects either misunderstanding of

the inputs to her subjective welfare, or the aim of wanting to impose one’s own

moral or aesthetic preferences on her? So one can’t just accept the Friedman

point and move on, without getting to a deeper set of issues that are not fully

captured merely by deciding to label oneself as a classical liberal, or for

that matter as a utilitarian.

Friday, April 14, 2017

Tax policy colloquium, week 11: Julie Cullen's "Political Alignment and Tax Evasion"

This past Monday, Julie Cullen presented her (coauthored)

paper, “Political Alignment and Tax Evasion," at the colloquium. (I had to put off blogging about it due to my

travel earlier this week.) It

intriguingly finds evidence (from IRS tax data) suggesting that people may

evade income tax more when they are politically opposed to the president.

Pretty much all of the effect comes from income that

is reported on Schedules C and E regarding income that is subject to neither

withholding nor information reporting.

Since evasion obviously can’t be observed directly (or at least, certainly

not through tax returns), it’s based on

the size of the tax gap.

Also, they obviously they can’t link tax evasion to individual

returns based on people’s (unknown) political views. So it’s based on county-level data. What they find is that, when a county has a

strong partisan lean in presidential election voting, the tax gap seems to be

bigger when a president of the other party is in office, as opposed to one of

the same party as that favored by the voters in that county. But the paper has a lot of sophisticated

controls that push one towards accepting the conclusion that people evade tax

more when they oppose the politics and policies of the current president.

Obviously, there is no data in the paper regarding tax

returns filed during the tenure of the current president. From other information in the paper I strongly

surmise (although the authors do not say) that its findings are driven mainly

by reduced tax compliance from Republicans when there are Democratic

presidents, rather than the reverse. This surmise reflects, for example, the fact

that there is an overall Republican lean to people who have the flexibility to

cheat more by reason of having a lot of Schedule C and E income as to which

there is no third-party reporting backup.

Leaving aside that aspect, one could regard the paper’s

main finding as either (a) so obviously true that it is unsurprising, or (b) so

counter-intuitive and surprising that one wonders if it can actually be true.

Why unsurprising?

We know from past research that attitudes towards government affect tax compliance,

and we know that partisan loyalties affect attitudes towards a particular government,

so via transitivity it seemingly had to be true.

Why

surprising? Well, the implication here

is that people who are reporting cash income add or drop a few hundred dollars

(say) from the amount that they report just because George W. Bush or else

Obama happens to be president and they like/dislike this particular individual

and his administration. That’s a

striking thought when one ponders it at the ground level, as something

that happens (at least in the aggregate) case by case.

A possible

payoff for policymakers would be that, purely on grounds of maximizing the

revenue yield relative to the cost of audits, Democratic presidents should

audit people in “red” counties more, and Republican presidents should audit

people in “blue” counties more. However,

this is unlikely to be considered an appealing takeaway for policymakers. So what it mainly does, within the tax

literature on compliance, is less a matter of providing useful policy payoffs than

of fleshing out our understanding of taxpayer behavior (i.e., regarding the

relevance of “tax morale” motives that are distinct from the Allingham-Sandmo

picture of financial optimization subject to risk aversion).

But it also

contributes to the political science literature, where the voting paradox

suggests that voters’ behavior must reflect consumption / expressive motives

rather than involving rational choice relative to the question of who will win

the election (since one’s time has value and one can only infinitesimally

affect the likely outcome).

On the road again

I'm back in NYC today after three days in Chicago, where I presented a paper at Northwestern Law School's Tax Policy Colloquium, and also took a bit of time off to revisit old stomping grounds (as I lived in Chicago from 1987-1995).

The paper I presented was "Interrogating the Relationship Between 'Legally Defensible' Tax Planning and Social Justice." I believe this paper is one of my more enjoyable reads, as most of it is written in the dialogue between two fictional individuals (who, in the undisclosed backstory that I had in mind when writing it, had liked each other romantically when they were younger, but never done anything about it and now have both moved on).

Slides for the talk are available here.

The paper I presented was "Interrogating the Relationship Between 'Legally Defensible' Tax Planning and Social Justice." I believe this paper is one of my more enjoyable reads, as most of it is written in the dialogue between two fictional individuals (who, in the undisclosed backstory that I had in mind when writing it, had liked each other romantically when they were younger, but never done anything about it and now have both moved on).

Slides for the talk are available here.

Friday, April 07, 2017

Polluted public discourse

I generally try to steer clear of political rants here, but it is striking how the likes of Paul Ryan and Marco Rubio combine delighted support when a Republican president bombs Syria, with opposing it and mocking its military ineffectuality when a Democrat does the same thing. They don't even try to appear consistent or principled, counting instead on voters' short memories and susceptibility to partisan stereotyping.

The Democrats are very far from wholly reciprocating, partly because they fear coming off as anti-military action, and partly because they still seem to imagine that there are neutral refs or other arbiters out there, whom they would benefit from pleasing as reasonable and sincere.

But the net effect is a huge tilt and bias in overall political discourse around presidents and foreign policy / military action - alongside the other bias, which almost always lies in favor of military action, be it wise or feckless, so that one will look "strong" rather than "weak."

The Democrats are very far from wholly reciprocating, partly because they fear coming off as anti-military action, and partly because they still seem to imagine that there are neutral refs or other arbiters out there, whom they would benefit from pleasing as reasonable and sincere.

But the net effect is a huge tilt and bias in overall political discourse around presidents and foreign policy / military action - alongside the other bias, which almost always lies in favor of military action, be it wise or feckless, so that one will look "strong" rather than "weak."

Wednesday, April 05, 2017

Discussion at NYU Law School of international tax paper by Mindy Herzfeld

Today at

NYU, Mindy Herzfeld presented her paper, The Case Against Tax Coordination:

Lessons from BEPS. I offered comments at the session, as did Mitchell Kane, and the following is

an expanded version of my notes.

As I read

it, the paper’s main three claims are as follows:

1) International

tax coordination, at least as represented by the OECD-BEPS project, is “problematic”

at best. This critique, however, combines calling the project (a) likely to be unsuccessful

on its own terms, and (b) illegitimate, or at least less legitimate than

claimed. These are quite distinct, in that one might especially regret (a) in

the absence of (b).

2) She

sees broader difficulties in tax coordination, in part because who gets a given

dollar of tax revenue is a zero-sum game.

3) She

views the BEPS project’s attempted implementation as slanted in favor of developed

countries &/or residence /production countries (which are not always the

same! – hence the equivocal U.S. response). There’s no global consensus to

allocate tax base to the place of production rather than the place of

consumption, & it’s not inherently the fairer approach of the two.

I have

some sympathy with Mindy’s views, although she’s more annoyed than I am by the self-righteous

rhetoric that inevitably accompanies a political process like BEPS. I’ll just make two broad points:

1) Since

who gets a given dollar of revenue is zero-sum, one has to look elsewhere for

gains from cooperation. But there are two places to look:

--Greater

efficiency from reduced waste that makes the overall pie larger.

--Loss

to someone else who’s outside the deal!

Residence

& source countries can potentially meet both by addressing profit-shifting

to tax havens. There’s some waste

associated with the profit-shifting, even though a lot of the underlying “activity”

is just paper-shuffling.

Plus,

while the havens don’t benefit from cutting out their role, suppose they’re

left outside the scope of the deal. Then there’s more room for the others to

benefit.

The fact

that I see a logical basis for cooperation from other countries cutting out the

tax havens doesn’t mean that I think the havens are doing anything wrong.

They’re rationally pursuing their own self-interest. This involves responding

to a type of consumer demand in the global marketplace. A place like the Cayman Islands isn’t

conniving in tax fraud by U.S. and other multinational companies – it’s simply

offering a convenient and trustworthy low-tax place to “park” profits, once

companies have exploited the other countries’ rules – which those

countries created, not the Caymans – to make the profit-shifting legally

effective in those countries.

But while,

on the one hand, I don’t see the Caymans as doing something wrong – it’s being

smart on behalf of their own human residents – they also don’t logically have a

place at the table if the other countries decide to revise their own rules in

such a way that the marketplace’s demand for what the Caymans is offering

declines.

2) Both

residence and source countries have reasonable goals. What puts them in

conflict is entity-level corporate income taxation.

I’d like

to redirect discussion, to a degree, from the question of “Which country gets

to tax the income?” to that of “What are differently situated countries trying

to do, and to what extent are their aims at least in principle reconcilable?”

I agree

that the definition of “source” isn’t going to resolve such questions as

whether the U.S. or India should tax profits from selling the fruits of U.S. IP

in India. It’s true that, in principle, income is an origin concept – it’s

about productive activity – while consumption is a destination concept – it’s

about using the fruits of economic production. So one might initially think, if

this were relevant to the global source issue, that production countries like

the U.S. have a stronger claim to tax the income.

But

there’s no particular reason why countries need to share tax base one way or

the other, depending on whether they claim to be using an income tax or not.

And in fact the U.S. income tax has a mix, not only of income and consumption

tax elements, but also (and separately) of origin-based and destination-based

source rules. E.g., royalties create US

source income if the property is used in the U.S., even if the IP was created

abroad.

Plus, of

course, policymakers in Washington are now debating a destination-based cash

flow tax that would replace the corporate income tax. A key reason for their

considering it is that it kinds of looks like an income tax, even though it

actually isn’t.

So let’s

shift to the question: What are differently situated countries trying to do?

Residence

or production countries – they might like to address tax competition with regard to where

production occurs, but that’s tough. Another goal is to succeed in taxing

resident individuals who are corporate owner-employees but avoid paying

themselves high salaries (instead, they profit through stock appreciation).

This is a big part of what motivates my concern about profit-shifting by U.S.

companies.

Source

or consumption countries – they might like to use monopsony power to extract some of the

profits that foreign multinationals could otherwise get from their

consumers. I have nothing against this

either. National self-interest relative

to the interests of outsiders is par for the course, plus a lot of the

multinationals are earning rents that reflect the market power they get, for

example, from IP protection. The exercise

of monopsony power doesn’t necessarily reduce global efficiency when it goes up

against monopoly power.

These

goals aren’t in principle completely inconsistent with each other, although

there’s no reason for production countries to be glad if a larger share of the

profits that their own resident individuals earn end up going instead to people

in the source countries.

But anyway,

two things are clear. First, we’re asking the corporate income tax to do more

work for different players than it really can these days. Second, we’re not as

ready to move away from it, and to shift its surviving functions to other tax

instruments, as one might like us to be.

Still fresh after all these years

I've been listening over the last couple of days to a fairly comprehensive Chuck Berry collection (available on Spotify), after his death brought his work back to mind. While I have listened to the originals before, it's probably been decades since I've listened to more than a couple at a time.

Perhaps I shouldn't have been, but I was startled by how consistently good the songs are (as well as the playing). Even though Berry was notorious for recycling riffs and tunes, he gives it a fresh twist each time (at least in the singles), through both the lyrics and his guitar work. The vignettes and (in effect) short stories that the songs embody are of course great - sometimes autobiographical, but at other times evidently channeling his audience rather than his own experiences, yet generally with a distinctive point of view that's often rooted in comic futility and frustration. Even the Beatles' and Stones' versions of his songs, while usually good (although the early Stones were a bit rudimentary), generally don't capture the self-confident wit.

Berry was almost thirty by the time he broke through, which adds to the surprise of his so brilliantly capturing the concerns of the white teenage audience that made him a star. A big part of the breakthrough was his combining blues and country to create a new style - great artistic advances often involve combining things that were already there - but the articulate humor and point of view were crucial as well.

Perhaps I shouldn't have been, but I was startled by how consistently good the songs are (as well as the playing). Even though Berry was notorious for recycling riffs and tunes, he gives it a fresh twist each time (at least in the singles), through both the lyrics and his guitar work. The vignettes and (in effect) short stories that the songs embody are of course great - sometimes autobiographical, but at other times evidently channeling his audience rather than his own experiences, yet generally with a distinctive point of view that's often rooted in comic futility and frustration. Even the Beatles' and Stones' versions of his songs, while usually good (although the early Stones were a bit rudimentary), generally don't capture the self-confident wit.

Berry was almost thirty by the time he broke through, which adds to the surprise of his so brilliantly capturing the concerns of the white teenage audience that made him a star. A big part of the breakthrough was his combining blues and country to create a new style - great artistic advances often involve combining things that were already there - but the articulate humor and point of view were crucial as well.

Tuesday, April 04, 2017

Tax policy colloquium, my 299th session (?): Kathleen Delaney Thomas, Taxing the Gig Economy

Yesterday, Kathleen Delaney Thomas presented Taxing the Gig Economy. Before getting to the very interesting topic, it has occurred to me recently to ask myself how many colloquium sessions I have done at NYU. I think the math goes as follows. This is Year 22. 14 sessions per year would mean 308 by the end of the semester and 294 before it began. But over the years I've missed one session due to illness, one due to a funeral, and one due to travel,. In addition, at least 2 were canceled due to weather (for papers by Yair Listokin and David Kamin - while a Saul Levmore session was also formally canceled due to snow, we got to hold it anyway).

If I'm not leaving out any missed sessions (such as further snow dates), that would mean I started this year at 289. Yesterday was session 10 for this year, so I suppose a milestone awaits. But it also means I've had a whole lot of micro-immersions over the years that give me a kind of backlog I find helpful. E.g., yesterday's paper was on a topic we've discussed at the colloquium previously, e.g., when Shu-Yi Oei presented a paper on what was then called the sharing economy, but is now (in a term I find more apt) more commonly called the gig economy.

The paper presents two interesting proposals regarding the taxation of certain workers who are not classified as employees for tax purposes. Instead, they are deemed to be independent contractors and thus, in effect, self-employed small business owners, which can present them with tax compliance challenges that they may be ill-equipped to meet.

Who is in this group? To start with, people who earn payments via platform companies such as Uber, Lyft, Task Rabbit, Airbnb, Etsy, etcetera. We may think of them as workers, but there's often property involved, such as the Uber driver's car, the Airbnb host's residence, and the Etsy seller's braided jute throw rug. (Also, Seamless? Stubhub? Craigslist? Square Card Reader? See below.) But one of the issues still open for analysis is to what extent the proposal might apply to non-employee service renderers and other small business owners who don't happen to connect with customers via platform companies.